How are Social Security Benefits Calculated

My article on Social Security last month spurred several good conversations with clients. It’s obviously a topic of great interest to many so I’m going to stick with it for at least a few more columns.

Have you ever wondered how your Social Security benefit is actually calculated? As with everything in personal finance and investing it seems, there is a lot of misinformation out there. In some ways it’s complicated, in others, not-so-much.

Basically, anyone with 10 years (or 40 quarters) of earnings is entitled to a Social Security benefit (some exceptions exist for certain government and railroad workers). To earn a quarterly credit, you must make at least $1,360 (or $5,440 for the year).

Ten years of credits is the minimum for Social Security eligibility, but the actual calculation of benefits is based on your highest 35 years of inflation adjusted earnings. For this reason, it’s important to review your Social Security statement to ensure the annual earnings on record are accurate.

Wage histories are always interesting to look at because they tell the story of person’s career trajectory. But they also illustrate the forces of inflation. Fortunately, Social Security recognizes the impact of inflation. When it’s time to apply for benefits, each year of earnings are adjusted to bring them into present day dollars for the final calculation.

Once the highest 35 inflation adjusted years of earnings are established, Social Security takes the average and applies it to the benefit formula.

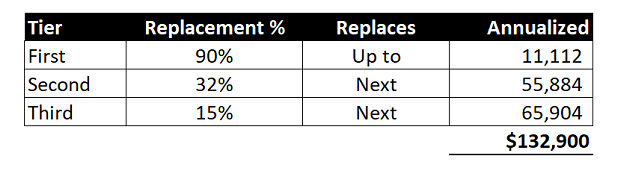

The formula is designed to replace a higher percentage of earnings for lower income workers. To achieve this, the benefit formula uses tiers. For 2019, the income replacement tiers are as follows:

In other words, Social Security is designed to replace 90% of your first $11,112 of average wages, 32% of the next $55,884 and finally, 15% of up to the next $65,904. Average wages above $132,900 do not count toward the benefit calculation. This ($132,900) is also the annual wage cap for income that is subject to FICA taxes.

Another way to think about this is if you hit the annual FICA wage cap through your entire career (assuming it was at least 35 years), you’d be eligible to collect the maximum Social Security benefit at full retirement age. The maximum benefit in 2019 for full retirement age is $2,861 per month (or $34,332 annually) which works out to slightly under 26% of the maximum indexed wage base.

Curiously, if you actually apply the benefit formula above you come up with a modestly higher number than $2,861. According to one of my Social Security references, this is due to several adjustments Social Security makes. Specifically, “timing of inflation adjustment calculations and the differences between the wage index used to calculate pre-age-60 adjustments, and CPI, which is used to calculate post-age-60 cost-of-living adjustments.”

There are a few key takeaways for individuals. First, remember that Social Security uses 35 years of earnings history to calculate an average. Any years of no earnings will result in a zero being part of your average which certainly will impact the benefit calculation.

Also, earnings above the first two tiers, about $67,000 ($11,112 + $55,884), only get a 15% weighting in the benefit formula. In other words, even though FICA taxes go all the way up to $132,900 in 2019, for the purposes of Social Security, the first $67,000 of earnings count a lot more than the next $65,900.

I hope that sheds some light on how Social Security benefits are calculated. If you have any questions about your own benefits or claiming strategies, don’t be shy about asking. I’ve purposely spent a lot of time on this subject to help people make the best decisions possible.

Trott Brook Financial is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.