The Illusion of Activity

As human beings, I think we’re naturally more inclined to be active than inactive. Our minds are constantly turning with thoughts and ideas. If you’ve never tried meditation, I would encourage it just to experience how difficult it is to keep your mind from drifting. You will be amazed at how challenging it is to “think about nothing” for even one or two minutes.

Taking action seems to be hardwired into our brains. When we see a problem or threat, our brain tells us to, “Do something!” Unfortunately, this human tendency is one that gets a lot of people in trouble when it comes to investing. Most people, in my experience, intuitively seem to believe that more activity equals better investment results. I would argue that generally speaking, the opposite is true; more activity leads to worse results.

This idea surely is counterintuitive (it’s remarkable how many things are in the investment game). But there is both empirical and high profile anecdotal evidence to support it.

The most famous research highlighting this concept is the ongoing Dalbar study. The study, which has been updated annually since 1994, seeks to highlight how investor behavior impacts returns. What is absolutely amazing is the results have been the same since year one, investors routinely realize significantly worse returns than the actual strategies they invest in.

For example, according to Dalbar, the S&P500 produced an average annual return of 9.85% over the 20 year period from 1995 – 2014. Yet the average equity investor studied only realized approximately 5.19% over the same period.

The Dalbar research shows that this phenomenon doesn’t have to do with asset selection (it didn’t matter if the investor chose index or active, large cap or small cap, etc.). The conclusion of the research, which again, hasn’t changed since 1994, is that the huge discrepancy is due to investor behavior. In other words, investors tend to make terrible decisions about when to buy and sell.

The poor decision making all comes back to fear and greed. Investors tend to sell when things go south and chase last year’s winners, both of which are recipes for disaster (selling low and buying high).

The Dalbar study clearly demonstrates that more activity has dramatically hindered investment performance. The subjects would have been far better off simply buying and holding (in other words, doing nothing).

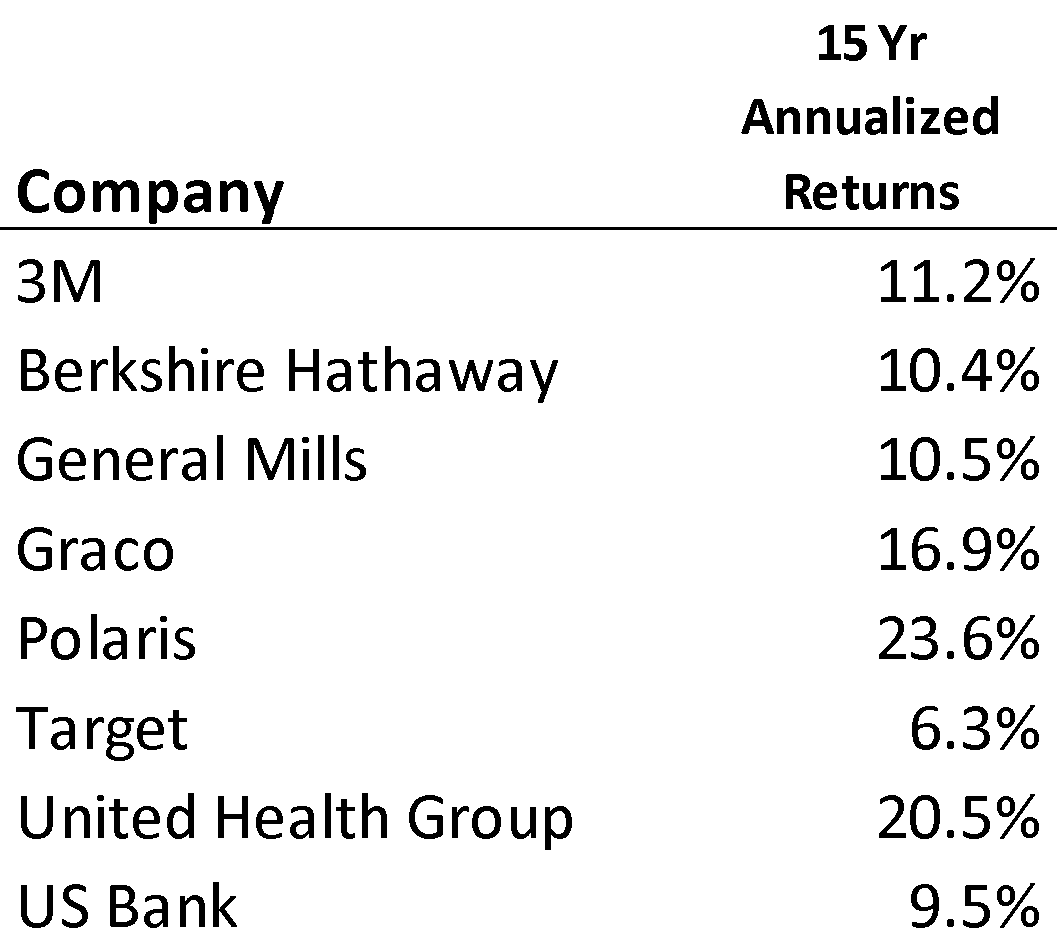

Let’s consider several interesting examples. The following table includes the average annualized stock performance of some recognizable companies for the years 2000 – 2014, including dividends. There’s nothing special about this list. I just chose a handful of names, mostly Minnesota based, that I thought people would be familiar with:

The 15 year period from 2000 – 2014 is especially notable because it contains two severe bear markets. The first came after the “Tech Bubble” burst in the year 2000. The second came in 2008 when the US entered “The Great Recession”.

During both bear markets, as measured by the S&P500, stocks broadly declined by approximately 50% (and none of these companies were immune to the market downturns). But here’s the important point, even with the two horrendous market declines, investors owning any of these positions 15 years ago would have had to do nothing but sit on their hands to capture these returns (no trading for 15 years). The same story is true for countless other publicly traded companies and strategies.

In previous memos, I’ve written about members of the Forbes 400 list (the richest 400 Americans). In the vast majority of cases, all of the wealth was generated by one asset. Here’s the current top 10:

|

Name |

Source of Wealth |

|

Bill Gates |

Microsoft |

|

Warren Buffett |

Berkshire Hathaway |

|

Larry Ellison |

Oracle |

|

Jeff Bezos |

Amazon.com |

|

Charles & David Koch |

Koch Industries |

|

Mark Zuckerberg |

|

|

Michael Bloomberg |

Bloomberg LP |

|

Jim Walton |

Wal-Mart |

|

Larry Page |

|

The point is, none of these people got rich actively trading. They got rich building great companies and holding them.

Remember Donald Sterling? He’s the disgraced former owner of the L.A. Clippers professional basketball team. Mr. Sterling bought the franchise originally in June of 1981 for $12.5 million according to the New York Times. Last year, he sold the team for $2 billion. When I first read about this, it blew me away. The math works out to a 15,900 percent rate of return!

What’s interesting though, if you annualize it over 33 years, it comes out to 16.6%. That number surprised me a bit. My gut instinct suggested the annualized figure was far higher. This demonstrates the power of compounding over time. But the more important lesson here is, from an investing standpoint, Mr. Sterling didn’t need to do anything for 33 years but hang on to an appreciating asset.

I’ll finish emphasizing my point with some additional anecdotal evidence from two of the most successful investors in history, Warren Buffett and his business partner Charlie Munger. Both Mr. Buffett and Mr. Munger have been long known for their “buy and hold” approach. Their company, Berkshire Hathaway, has owned many stocks for decades. Those include names like Wells Fargo, Coca-Cola and American Express. Obviously things have worked out well.

Here are a few of my favorite quotes around the issue of holding periods and frequent trading. The first is an excerpt from Mr. Buffett’s 1988 letter to shareholders:

“When we own portions of outstanding businesses [stocks for example] with outstanding managements, our favorite holding period is forever (emphasis added). We are just the opposite of those who hurry to sell and book profits when companies perform well but who tenaciously hang on to businesses that disappoint. Peter Lynch aptly likens such behavior to cutting the flowers and watering the weeds.”

Another more humorous quote attributed to Buffett is as follows:

“Calling someone who trades actively in the market an ‘investor’ is like calling someone who repeatedly engages in one-night stands a romantic.”

Buffett’s long-time business partner, Charlie Munger, often known for his forthright style of speaking also has a number of memorable quotes on the topic of active trading. At the 2000 Berkshire Hathaway Annual shareholders meeting, Mr. Munger famously introduced the concept of “sit on your ass” investing. Emphasizing the difficulty of consistently buying and selling at the right time, Mr. Munger said:

“If you buy a business just because it’s undervalued, then you have to worry about selling it when it reaches its intrinsic value. That’s hard. But if you can buy a few great companies, then you can sit on your ass…that’s a good thing.”

Obviously Mr. Buffett and Mr. Munger are simplifying their philosophy in the above quotes. A lot of work still goes into a buy and hold approach. Buffett speaks to this as well in the 1988 letter to shareholders:

“We continue to concentrate our investments in a very few companies that we try to understand well (emphasis added).”

The last part of that final quote is key. It should go without saying that researching an opportunity upfront and making the initial investment are only the beginning. Staying on top of a company for example, and “understanding it well,” takes time. Unfortunately, these efforts easily go unrecognized with a buy and hold approach.

I wrote this memo because Jim and I are frequently asked by clients about making changes. Additionally, we’ve received some feedback from recent surveys basically saying, “I wish you would trade more.” I believe this sentiment all comes back to how I began this memo; human beings are naturally inclined to “take action,” even when none is needed. Surely financial media, such as CNBC, which is hyper-focused on the news of the day also add to the idea that investors need to be “doing something” all of the time. Unfortunately, in the investment game, trading activity more often than not just creates the illusion of progress.

In fact, in my experience (and Jim and I regularly chuckle about this), people who basically don’t pay attention to their investments seem to capture better returns than those who do. This shouldn’t come as much of a surprise based on everything we’ve discussed. The individuals who are regularly watching their accounts are obviously the ones who are most likely to “do something” at the worst possible time.

Investors are usually their own worst enemy, and this is really evident in the Dalbar research. Throughout my career, I’ve come to learn that financial advisors don’t create most of their value in the investment advice they give (what to buy). Where we create the most value, by far, is helping clients avoid extremely costly mistakes and, without a doubt, being overly active is a mistake. So next time you wonder what your financial advisor is “doing” for you, just remember that convincing you to “do nothing” very well could be the best advice.

1The S&P 500, or the Standard & Poor's 500, is an American stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ

2http://www.thinkadvisor.com/2015/04/21/bad-behavior-cost-mutual-fund-investors-8-percenta

3Past performance is not indicative of future results.

4JP Morgan “Guide to the Markets”. https://www.jpmorganfunds.com/cm/Satellite?UserFriendlyURL=diguidetomarkets&pagename=jpmfVanityWrapper

5http://www.forbes.com/forbes-400/list/#version:static_header:position